“If you’re moving your startup to the U.S. and sitting on a pile of USDC, the conversion process is straightforward — but the tax and timing nuances can trip you up if you’re not careful.” That’s the blunt assessment from Elena Torres, a crypto tax partner at Deloitte’s San Francisco office. She’s right. For the thousands of international founders who have raised capital in stablecoins like USDC, landing in the U.S. with a wallet full of digital dollars is both a blessing and a logistical puzzle.

You’ve got the funding. You’ve got the visa. Now you need to turn that USDC into actual greenbacks to pay rent, salaries, and AWS bills. The good news? The infrastructure is mature. The bad news? Fees, slippage, and regulatory paperwork can eat into your runway if you don’t plan ahead.

Why USDC? And Why Now?

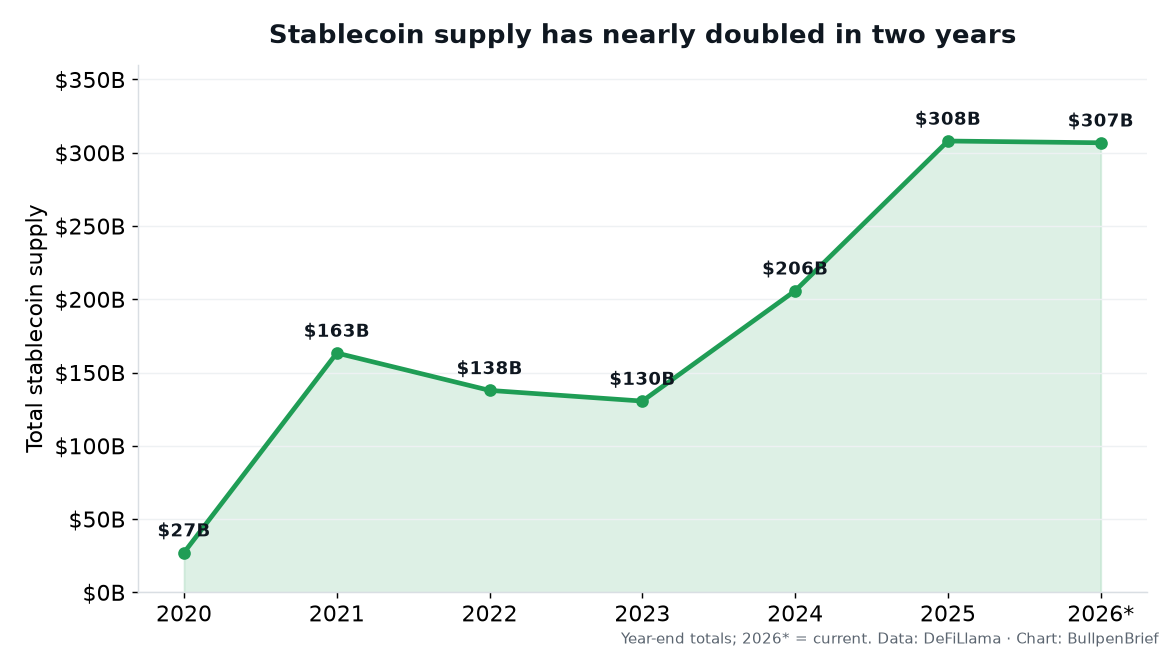

USDC — the second-largest stablecoin by market cap at roughly $34 billion as of March 2025 — is pegged 1:1 to the U.S. dollar, issued by Circle and backed by cash and short-term Treasuries. It’s the default on-ramp for many crypto-native startups, especially those raising from global VCs who prefer to move capital without traditional wire delays.

But a stablecoin isn’t legal tender. You can’t hand a USDC token to your landlord or the IRS. So the moment your startup establishes a U.S. bank account — typically a business checking account at a bank like Mercury, Chase, or Silicon Valley Bank — the conversion game begins.

Marcus Webb, BullpenBrief — I’ve watched dozens of founders navigate this. The core question is: Where do you convert, and how do you minimize the friction? Let’s break it down by the three main routes.

Route 1: Centralized Exchanges — The Retail Path

Coinbase, Kraken, Gemini — these are the obvious choices. You send USDC from your wallet to the exchange, sell it for USD, and withdraw to your linked bank account. Coinbase, for instance, charges zero fees on USDC-to-USD conversions for institutional accounts, but retail users still face a spread of about 0.1% to 0.5% depending on volume.

“For a startup moving $500k or more, the spread on a retail exchange is a rounding error — but the withdrawal limits can be a headache. Most exchanges cap daily wire transfers at $250k unless you’re on a dedicated OTC desk.”

— James Park, head of corporate accounts at Kraken

If you’re a solo founder with less than $100k, this route works fine. But for larger sums, the OTC desk becomes essential.

Route 2: OTC Desks — The Institutional Play

Over-the-counter (OTC) trading desks like Cumberland, Genesis (pre-bankruptcy, now restructured), or even Coinbase Prime offer direct block trades. You negotiate a fixed price for your USDC, usually at a slight premium or discount to $1.00 depending on market depth. OTC desks typically settle via bank wire within one business day.

The advantage? No slippage, no market impact, and no daily withdrawal caps. The catch? Minimums start at $100,000, and you’ll need to complete KYC/AML checks that can take 48–72 hours. For a startup that just closed a $2 million seed round, this is the most capital-efficient path.

Tax Implications: The Silent Runway Killer

Here’s where many founders trip. Converting USDC to USD is a taxable event in the U.S. — even though the stablecoin is pegged 1:1. The IRS treats USDC as property, so any gain or loss relative to your cost basis is reportable. If you received USDC at $1.00 and sell at $1.00, your gain is zero — but you still need to file Form 8949 with every transaction.

“Founders often assume stablecoin conversions are tax-free. They’re not. The IRS requires reporting, and if you’ve been swapping USDC for ETH or using DeFi protocols, your cost basis gets messy fast,” warns Sarah Lin, a crypto-focused CPA at Lin & Associates in New York.

Practical advice: Use a crypto tax software like Koinly or CoinTracker to track every USDC inflow and outflow. If you’re converting $500k in one lump sum, the tax paperwork is minimal. But if you’ve been farming yield on Aave or staking USDC on Compound, each transaction adds complexity.

The Banking Bottleneck — and How to Beat It

Even after you convert to USD, the money isn’t truly available until it lands in your bank account. ACH transfers from exchanges take 1–3 business days. Wires are faster (same-day if initiated before cutoff) but often incur $20–$30 fees. For a startup needing to pay a $50k AWS bill tomorrow, that delay matters.

Some founders use a “hybrid” approach: convert a portion to USD via Coinbase, leave the rest in USDC on a self-custodial wallet, and use a crypto debit card (like the Coinbase Card or BitPay) for smaller expenses. But those cards have daily limits (typically $10k–$25k) and may not be accepted for large vendor payments.

Another option: Circle’s own Circle Account. Circle allows businesses to hold USDC and convert to USD at par with no fees, then withdraw via wire or ACH. The catch? You need to qualify as an institutional client — minimum $250k in monthly volume. For a startup that hasn’t yet hit that threshold, this door is closed.

Regulatory Hurdles: FinCEN, State Licenses, and Travel Rules

If you’re converting USDC for your own personal account, the regulatory burden is light. But if you’re a startup founder converting on behalf of the company — especially if your company is a Delaware C-corp — you need to ensure your exchange account is registered as a business entity. Many exchanges require a separate business account with enhanced due diligence.

Also, be aware of the “Travel Rule” for transactions over $3,000. Exchanges must share customer information with counterparties. For a founder moving $1 million, expect a call from the exchange’s compliance team asking for proof of funds and source of wealth.

Bottom line: The conversion from USDC to USD is technically simple but strategically complex. Choose your route based on volume, speed, and tax readiness.

What’s Next? The Stablecoin Regulatory Shift

The stablecoin landscape is about to change. In February 2025, the U.S. Senate Banking Committee advanced the Stablecoin Transparency Act, which would require all issuers to hold fully liquid reserves and undergo monthly audits. If passed, USDC’s trust premium could widen — making it even easier to convert at par with banks.

Meanwhile, the Federal Reserve is testing a “tokenized deposit” system with several banks, potentially allowing stablecoins to settle directly on FedNow rails. If that goes live in 2026, converting USDC to USD could become as instant as a Venmo transfer.

For now, the best advice for a startup founder moving to the U.S. is simple: open a U.S. bank account before you arrive, set up an institutional exchange account with OTC access, and hire a crypto-savvy accountant. The dollars are waiting — but the paperwork isn’t going to do itself.