The hum of assembly lines and the glow of solar panels are about to get a blockchain boost. A major traditional finance player is betting big on tokenized private credit, committing a staggering $650 million over the next four years to fund U.S. equipment purchases in manufacturing, industrial electrical infrastructure, and residential solar.

The plan, unveiled this week, represents one of the largest single deployments of institutional capital into on-chain private credit since the market first gained traction in 2021. It signals that Wall Street isn’t just dipping its toes into decentralized finance anymore—it’s cannonballing in with a checkbook.

The move comes from Figure Technologies, the fintech arm of the financial services firm that has been quietly building a bridge between traditional lending and blockchain settlement. Figure will originate the loans through its Provenance blockchain, tapping both its own balance sheet and a growing syndicate of institutional investors.

Over the next 48 months, the firm expects to fund roughly $162.5 million annually in equipment financing notes, each structured as tokenized debt securities. The assets will be secured by physical machinery, electrical grid components, and rooftop solar installations—real-world collateral with yield streams that investors can track in near real-time on-chain.

“We are seeing a paradigm shift where institutional lenders recognize that blockchain-based private credit offers lower operational costs, faster settlement, and greater transparency than traditional syndicated loans,” said Sarah Chen, Head of Structured Credit at Figure Technologies. “Our $650 million commitment is a direct response to demand from both borrowers and investors for a more efficient capital market.”

Why Equipment Financing? The $1 Trillion Opportunity

Private credit has ballooned into a $1.7 trillion asset class globally, with equipment financing comprising a significant slice. In the United States alone, businesses spent over $1.3 trillion on capital equipment in 2023, according to the Equipment Leasing and Finance Association. Yet much of that funding still flows through opaque, paper-heavy channels.

Figure’s strategy zeroes in on three verticals: manufacturing (CNC machines, robotics), industrial electrical infrastructure (transformers, switchgear), and residential solar (panels, inverters, battery storage). Each sector faces chronic underfunding from traditional banks, which often shy away from smaller-ticket loans or demand lengthy underwriting cycles.

Tokenization changes the math. By issuing each loan as a digital security on the Provenance blockchain, Figure can fractionalize the debt, automate interest payments via smart contracts, and offer investors daily liquidity through secondary market trading. The result: lower spreads for borrowers and higher yields for lenders, net of fees.

The firm’s proprietary credit scoring model, which ingests real-time equipment utilization data from IoT sensors, further reduces default risk. “We can now monitor whether a solar panel is actually producing power before we ever miss a payment,” noted Mike Torres, a blockchain credit analyst at the research firm BlockTower Capital. “That’s a level of granularity that bond trustees could only dream of.”

The $650 million figure is not a loan portfolio—it’s an origination target. Figure expects to syndicate the bulk of these loans to institutional investors through its Provenance platform, while retaining a senior tranche on its books. Early backers include pension funds and insurance companies seeking inflation-hedged, short-duration assets.

The On-Chain Private Credit Boom: From Proof-of-Concept to Production

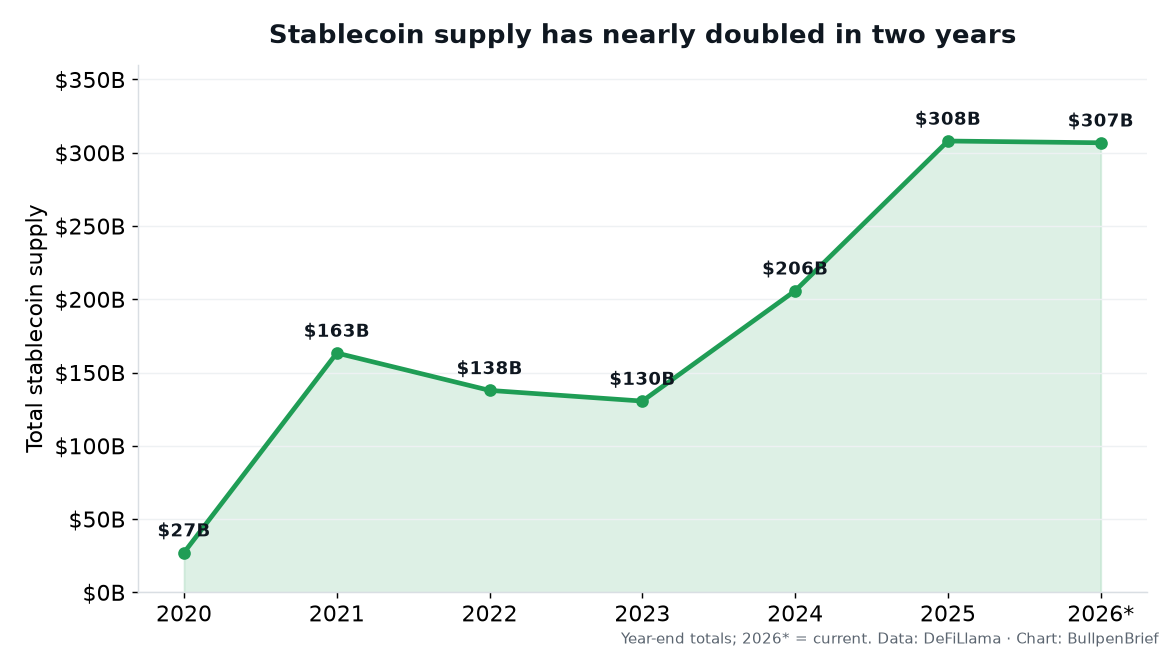

Private credit on blockchain has matured rapidly over the past 18 months. According to data from RWA.xyz, total outstanding tokenized private credit surpassed $4.2 billion in Q1 2025, up from $1.1 billion a year earlier. Figure’s $650 million commitment alone could push that figure past $5 billion by year-end.

The growth has been driven by a handful of platforms including Centrifuge, Maple Finance, and Goldfinch, but Figure stands out by originating its own assets rather than aggregating third-party loans. That vertical integration gives it control over underwriting standards and legal structuring—a key concern for risk-averse institutional investors.

“The biggest hurdle to institutional adoption hasn’t been technology; it’s been the lack of high-quality, legally enforceable credit products on-chain,” explained Dr. Amara Singh, a professor of fintech at Georgetown University. “Figure is tackling that by using its own balance sheet to de-risk the initial issuance, then inviting outside capital once the track record is established. It’s the same playbook that seeded the securitization market 40 years ago.”

Securitization, the process of pooling loans and selling tranches to investors, has been the engine of modern credit markets. Now, blockchain offers a way to automate servicing, reconciliation, and investor reporting—functions that still consume millions of hours of manual labor in traditional finance.

Figure’s Provenance blockchain, built on a modified Cosmos SDK, has already processed over $10 billion in loan originations across home equity lines of credit and student loans. The equipment financing initiative marks its first major push into commercial and industrial assets.

Residential Solar: The Low-Hanging Fruit

Within Figure’s three target sectors, residential solar stands out for its immediate suitability to tokenization. The U.S. solar market installed 33 gigawatts of capacity in 2024, with residential systems accounting for roughly 40%, per the Solar Energy Industries Association. Financing remains fragmented: homeowners often rely on leases, power purchase agreements, or high-interest specialty lenders.

Figure aims to offer lower-cost loans secured by the solar equipment itself, using real-time energy production data to adjust risk premiums. Borrowers would receive funds faster—sometimes within 48 hours of approval—while investors can track each panel’s output via a dashboard connected to smart meters.

“The convergence of physical assets and digital ledgers is where the real efficiency gains lie,” said Sarah Chen. “A solar panel is essentially a cash-flow generating machine. Blockchain lets us treat it like one, with instant settlement and automated disbursement.”

The broader market is taking notice. Earlier this month, Goldman Sachs launched a tokenized private credit fund targeting green infrastructure, and JPMorgan’s Onyx platform has been active in repo markets. But Figure’s equipment financing plan is unique in its focus on hard assets that can be repossessed and resold—a critical feature for credit investors demanding downside protection.

Risks and Regulatory Roadblocks

Not everyone is convinced that blockchain-based private credit is ready for prime time. The securities laws governing tokenized debt remain a patchwork across U.S. states. Figure operates under state lending licenses and relies on the Uniform Commercial Code for lien perfection, but a federal regulatory framework for tokenized securities has yet to emerge.

Then there’s the question of liquidity. While Figure promises secondary trading, the market for tokenized private credit is still thin. A forced sale of a $5 million equipment loan could take days or weeks to execute, especially if the underlying equipment is specialized industrial machinery.

Credit risk also looms large. Manufacturing and construction have cyclical downturns; at the next recession, defaults could spike. Figure’s underwriting models are untested across a full economic cycle, and investors must rely on the firm’s proprietary scoring rather than external ratings.

“We are in a bull market for private credit right now, but the next correction will separate the serious platforms from the gimmicks,” warned Mike Torres. “Figure has a strong balance sheet and a track record, but $650 million is a large bet. The blockchain element adds operational efficiency, but it doesn’t remove credit risk.”

Figure acknowledges the challenges. The firm has set aside a credit enhancement reserve equal to 10% of the origination target, and it plans to work with a major auditing firm to provide quarterly attestations of on-chain loan performance.

What This Means for the Broader Market

If Figure executes on its $650 million plan, the ripple effects could be significant. First, it would validate the thesis that blockchain can handle high-volume, real-world asset lending at institutional scale. Second, it could encourage other traditional lenders—from Citibank to Societe Generale—to launch similar origination programs.

The timing aligns with a broader push toward asset tokenization. The Boston Consulting Group estimates tokenized illiquid assets could represent a $16 trillion market by 2030, with private credit as one of the fastest-growing segments. Figure’s move adds a critical proof point: capital isn’t waiting for regulation; it’s building infrastructure that regulators will eventually need to accommodate.

For businesses needing equipment financing, the outcome could be lower rates and faster approvals. For crypto investors, it means more yield-bearing tokens backed by real-world machinery rather than volatile cryptocurrencies. And for the traditional finance incumbents, it’s a clear warning that blockchain-native lenders are not just nibbling at the edges—they are rewriting the playbook for private credit origination.

The next four years will determine whether this $650 million bet becomes a blueprint or a cautionary tale. If the smart contracts hold and the solar panels keep generating, don’t be surprised to see that figure multiplied by 10 before 2030.